With the introduction of tariffs on Tuesday, there is significant uncertainty across all sectors regarding the potential outcome. While important data releases—including the PCE Index, Personal Income & Spending, and Consumer Sentiment for the quarter—have taken place, their impact is expected to be largely overshadowed by apprehension surrounding the widespread tariff decisions.

With the upcoming release of inflation reports, including the CPI and PPI this week, all eyes will be on these two key metrics. The focus remains on tariffs and their impact on the markets, as well as inflation, which is likely to be influenced by the new tariff policies.

PCI Index

A separate measure of prices known as the core rate rose a sharper 0.4% in February, a tick above Wall Street’s forecast. The increase in the core PCE in the past year climbed to 2.8% from 2.7%. The core rate omits food and energy prices, which often jump up and down in the short run. It’s seen as a better predictor of future inflation.

Consumer Spending

Consumer spending rose a modest 0.4% last month, the government said, and rebounded from a decline in January. Economists surveyed by The Wall Street Journal had projected a 0.5% gain. Household spending is the main engine of the U.S. economy, but it appears to have sputtered in early 2025.

Consumer Sentiment

The final reading of consumer sentiment in March fell to a 32-month low, as more Americans than at any time since the financial crisis think unemployment will rise in the year ahead. The second of two readings of the consumer-sentiment survey fell to 57.0 from an initial 57.9, the University of Michigan said Friday.

Primary Mortgage Market Survey Index

• 15-Yr FRM rates saw an increase of 0.06% with the current rate at 5.89%

• 30-Yr FRM rates saw a decrease of -0.02% with the current rate at 6.65%

MND Rate Index

• 30-Yr FHA rates saw an increase of 0.03% for this week. Current rates at 6.18%

• 30-Yr VA rates saw an increase of 0.03% for this week. Current rates at 6.20%

Jobless Claims

Initial Claims were reported to be 224,000 compared to the expected claims of 226,000. The prior week landed at 225,000.

What’s Ahead

CPI and PPI are ahead next week as well as the tariffs, which are set to be in effect starting Tuesday.

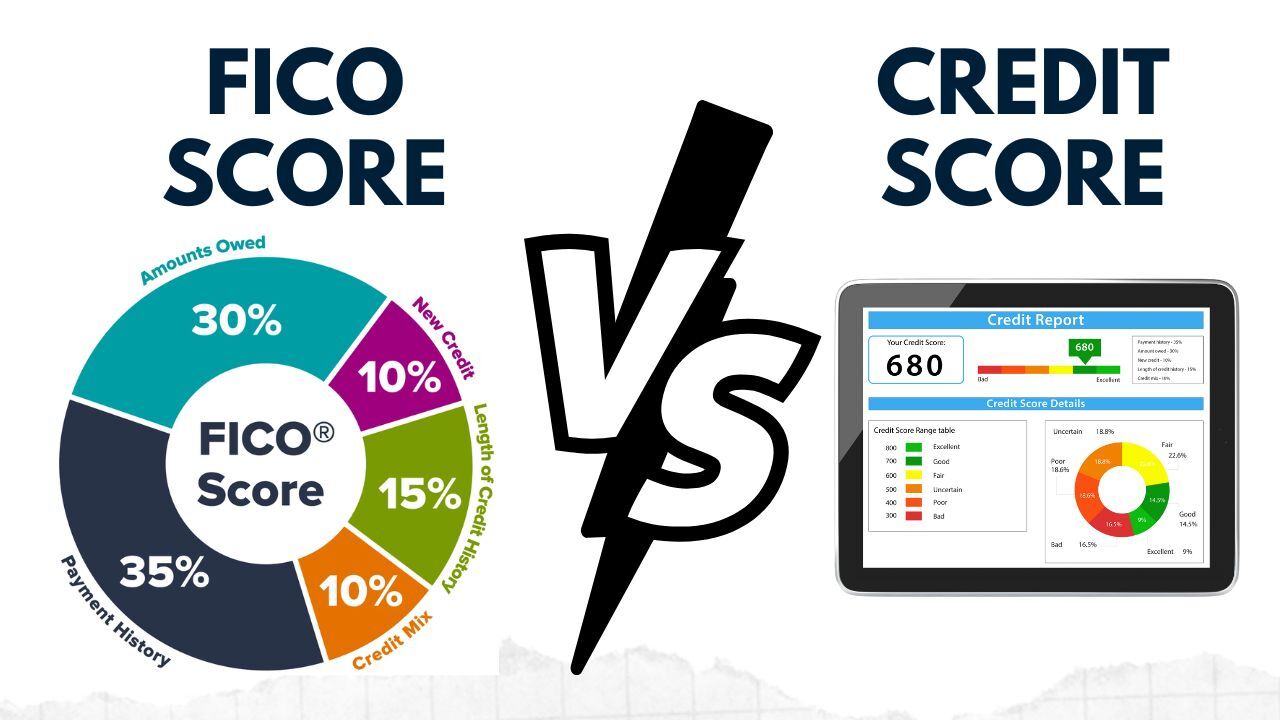

When applying for a mortgage, your creditworthiness plays a significant role in determining your loan approval and interest rates. Two commonly referenced terms are FICO score and credit score, which are often used interchangeably but have distinct differences.

When applying for a mortgage, your creditworthiness plays a significant role in determining your loan approval and interest rates. Two commonly referenced terms are FICO score and credit score, which are often used interchangeably but have distinct differences.