Renting can provide flexibility during career growth, relocation, or life transitions. However, when renters begin preparing for homeownership, the shift requires more than saving for a down payment.

Renting can provide flexibility during career growth, relocation, or life transitions. However, when renters begin preparing for homeownership, the shift requires more than saving for a down payment.

Moving from renter to homeowner introduces new financial responsibilities and underwriting standards. Understanding how lenders evaluate housing history, credit behavior, and reserve strength allows renters to transition confidently into mortgage qualification.

Track Rent Payment History Carefully

Consistent, on-time rent payments demonstrate financial discipline and housing reliability. While rent does not always appear on traditional credit reports, lenders may request verification from landlords or documentation through bank statements. Maintaining clear proof of payment strengthens your application profile and supports your ability to manage future mortgage obligations responsibly.

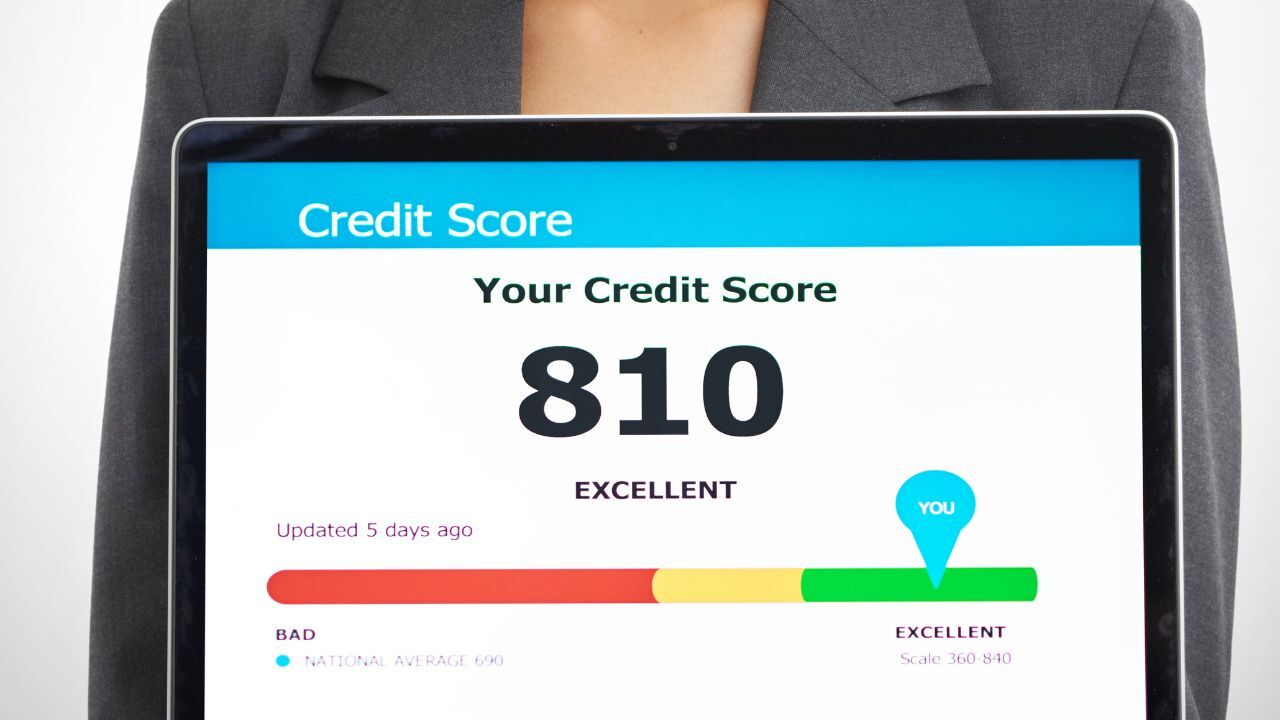

Strengthen Credit Before Applying

Many renters rely on revolving credit for flexibility. High utilization balances or inconsistent payment timing can impact qualification and loan pricing. Reducing revolving balances below key utilization thresholds and maintaining strong on-time payment history improves overall credit positioning. Reviewing credit reports several months before applying provides time to correct errors or address weaknesses.

Build More Than a Down Payment

A down payment is only one component of readiness. Buyers must also plan for closing costs, prepaid taxes, insurance deposits, and moving expenses. Additionally, lenders may require documented reserves equal to several months of housing payments. Entering homeownership with minimal liquidity increases vulnerability. A financial cushion strengthens long-term stability.

Prepare for the True Cost of Ownership

Rent payments typically include maintenance handled by a landlord. Homeownership introduces direct responsibility for repairs, property taxes, and insurance. Budgeting realistically for these additional obligations prevents payment shock. Creating a projected monthly housing budget before closing improves confidence.

Avoid Major Financial Changes Before Closing

Opening new credit accounts, financing vehicles, or making large purchases before closing can alter debt-to-income ratios and jeopardize approval. Maintaining financial consistency throughout the underwriting process is critical. Stability supports successful closing.

Understand Underwriting Expectations

Lenders evaluate income consistency, employment stability, credit history, and debt ratios collectively. Preparing documentation early reduces stress and shortens processing timelines.

Transitioning from renting to owning represents a meaningful financial milestone. With structured preparation and clear understanding of mortgage expectations, renters can enter homeownership with confidence.

If you are preparing to move from renting to owning and want to evaluate your mortgage readiness thoroughly, reach out to review your financing strategy with clarity and long-term focus.

Buying a home is one of the most exciting goals you can set, but your credit score plays a major role in how easy or challenging the process will be. The good news is that with time and planning, you can strengthen your credit and set yourself up for a smoother approval when you are ready to buy next year.

Buying a home is one of the most exciting goals you can set, but your credit score plays a major role in how easy or challenging the process will be. The good news is that with time and planning, you can strengthen your credit and set yourself up for a smoother approval when you are ready to buy next year.