Inflation is a topic that impacts nearly every part of the economy, from the cost of groceries to long term financial planning. For homeowners and those considering a mortgage, inflation can feel intimidating. However, with the right perspective and strategies, borrowers can use inflation to their advantage and create lasting financial benefits.

Inflation is a topic that impacts nearly every part of the economy, from the cost of groceries to long term financial planning. For homeowners and those considering a mortgage, inflation can feel intimidating. However, with the right perspective and strategies, borrowers can use inflation to their advantage and create lasting financial benefits.

Understanding the Relationship Between Mortgages and Inflation

Inflation reduces the purchasing power of money over time. While this can make everyday expenses higher, it also works in favor of borrowers with fixed rate mortgages. Since the mortgage payment stays the same each month, the real value of that payment decreases as wages and prices rise. In other words, the loan feels more affordable as time passes.

The Benefit of Fixed Rate Mortgages

One of the clearest ways to benefit from inflation is by choosing a fixed rate mortgage. Unlike adjustable-rate loans, fixed rate options lock in the interest rate for the entire term. As inflation increases, homeowners with fixed mortgages enjoy stable payments while renters often face rising rents. Over the years, this stability can free up more of the household budget for savings, education, or other investments.

Building Equity Faster

Inflation can also accelerate the growth of home equity. As home values rise along with inflation, homeowners often see their property appreciate. While the mortgage balance gradually decreases with each payment, the value of the asset typically grows, creating a stronger financial position. For families, this can mean greater security and more options for the future.

Protecting Long Term Wealth

Real estate has long been considered a hedge against inflation. By owning a home with a stable mortgage, borrowers can protect themselves from some of the challenges that rising costs bring. Monthly payments remain consistent, while the property itself may increase in value over time, helping homeowners preserve and even grow their wealth.

Inflation can create challenges in daily life, but it also presents an opportunity for homeowners. By securing a fixed rate mortgage and thinking long term, borrowers can position themselves to benefit as inflation reduces the real cost of their loan and increases the value of their property.

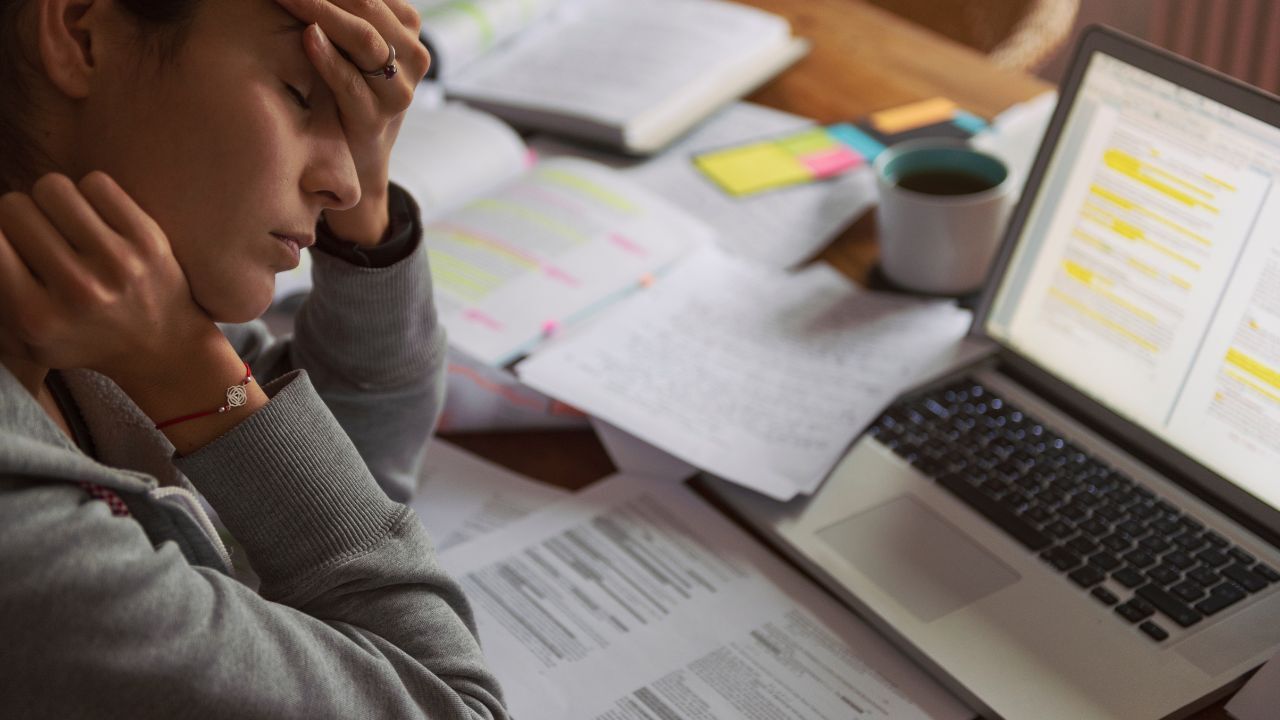

Buying a home is one of the most exciting milestones in life, but it can also be one of the most exhausting. From house hunting and comparing loan options to managing the financial paperwork and deadlines, the process can become overwhelming. Mortgage burnout happens when the stress and demands of the home buying journey begin to wear you down, making it harder to stay focused and positive. The good news is there are ways to protect yourself from burnout and keep the process manageable.

Buying a home is one of the most exciting milestones in life, but it can also be one of the most exhausting. From house hunting and comparing loan options to managing the financial paperwork and deadlines, the process can become overwhelming. Mortgage burnout happens when the stress and demands of the home buying journey begin to wear you down, making it harder to stay focused and positive. The good news is there are ways to protect yourself from burnout and keep the process manageable.