When you are ready to buy a home, it is natural to shop around for the best mortgage rate and terms. But you may have heard that submitting multiple loan applications can damage your credit score and throw a wrench in your homebuying plans. Here is the truth behind hard inquiries, rate shopping, and how to protect your credit while securing the best deal.

When you are ready to buy a home, it is natural to shop around for the best mortgage rate and terms. But you may have heard that submitting multiple loan applications can damage your credit score and throw a wrench in your homebuying plans. Here is the truth behind hard inquiries, rate shopping, and how to protect your credit while securing the best deal.

Understanding Hard Inquiries vs. Soft Inquiries

Whenever a lender runs your credit, whether for a credit card, auto loan, or mortgage, they generate a hard inquiry on your report. Hard inquiries can lower your score by a few points and typically stay on your report for up to 12 months, but they fade after about two years. Alternatively, if you check your own credit or prequalify through some websites that promote no affect to your credit score, it will generate a soft inquiry and will not affect your score.

Rate Shopping Grace Periods

Credit scoring models from FICO and VantageScore recognize that savvy borrowers comparison-shop for the same type of loan. To prevent penalizing you for smart shopping, they group multiple mortgage (and auto) inquiries within a short window, usually 14 to 45 days, and will count them as a single inquiry. This means you can apply to several lenders within a couple of weeks without a significant hit.

- FICO: 14-day window for newer models; 45 days for older versions.

- VantageScore: 14-day window across all versions.

How Much Will Your Score Drop?

You can expect a single hard inquiry to typically cost you 5–10 points on a FICO score. If you keep all your mortgage applications within the allowed window, they will count as one inquiry and only incur that initial drop. If you miss the 14-day window applying for several loans over a 2-month period, you can expect it to trigger multiple inquiry hits, intensifying the effect.

Keep in mind that there are other factors that will play into this like credit utilization, payment history, length of credit history, and more that will carry more weight than a handful of inquiries. If your overall credit profile is strong, a temporary 5–10 point drop will not usually affect the outcome of the loan.

Best Practices for Mortgage Shoppers

- PreQualify First: Work with a mortgage professional that uses soft pull prequalification tools to see your likely rates without affecting your score.

- Apply Quickly: Have a plan in place to aggressively shop within a two-week span to bundle inquiries into one.

- Check Your Credit: Review your credit report before applying to correct any errors (e.g., misreported late payments, incorrect balances, accounts that you do not recognize, etc.).

- Mind Your Other Credit: Avoid opening new credit cards or taking out auto loans during this window; they generate hard pulls too. It’s best to refrain from any purchases during the approval process.

- Lock in Your Rate: Once you find a competitive offer, lock your rate to avoid having to re-apply and ensure your hard inquiry clock stops.

Multiple mortgage applications will hurt your credit if they are spread out over too long a period. By focusing your shopping within the 14-day window, you will only face a single, minor score dip. Pair smart timing with a strong credit profile, and you can secure the best mortgage deal without sacrificing your score.

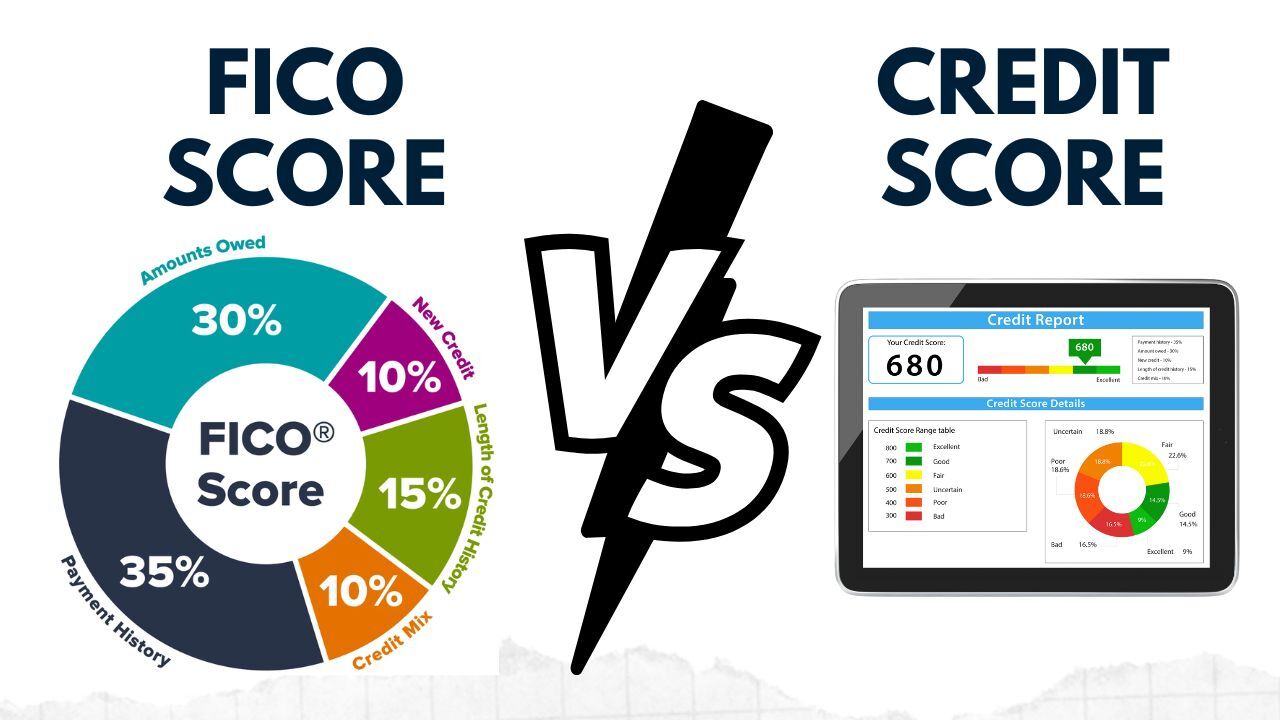

When applying for a mortgage, your creditworthiness plays a significant role in determining your loan approval and interest rates. Two commonly referenced terms are FICO score and credit score, which are often used interchangeably but have distinct differences.

When applying for a mortgage, your creditworthiness plays a significant role in determining your loan approval and interest rates. Two commonly referenced terms are FICO score and credit score, which are often used interchangeably but have distinct differences.